The Midas Touch Gold Model™ Update

As usual, we would like to present you with an up-to-date overview of the Midas Touch Gold Model™ and Florian Grummes’ short- to medium-term outlook. Our dear friends from Incrementum will publish this update in their upcoming In Gold We Trust report 2025. May 6th, 2025: The Midas Touch Gold Model™ Update.

The Midas Touch Gold Model examines the gold market from various perspectives with a rational and holistic approach, standing out for its versatility and quantitative measurability. Despite the abundance of data, the model succeeds in presenting a comprehensive and in-depth analysis clearly and concisely in a table, allowing for precise conclusions to be drawn.

Gold – The big picture

Auro loquente omnis oratio inanis est.” – “When gold speaks, the world is silent. – Latin proverb

Just a few days after reaching a new all-time high at USD 3,500, the Midas Touch Gold Model™ abruptly shifted from bullish to bearish on April 30th, 2025. The sharp price correction triggered numerous signal changes among the monitored indicators. Following the record rally and temporary excesses of recent weeks, a seasonally typical correction or consolidation into June would not only be healthy but also expected. If Chinese investors resume or even directly continue their buying spree, prices above USD 4,000 remain quite possible later in the year. Silver and mining stocks, however, are still lagging and require continued patience.

The Midas Touch Gold Model™ switched from bullish to neutral on April 15th, 2024, allowing it to promptly identify the trend reversal in the gold market following the new all-time high at USD 2,431. Typically, the ongoing pullback should soon or later lead the gold price back to the breakout level in the range of approximately USD 2,075 to USD 2,150. Following such a healthy consolidation, the bull market is expected to gain momentum, with price targets surpassing USD 3,000. At that point, mining stocks are poised to finally catchup and then surge ahead.

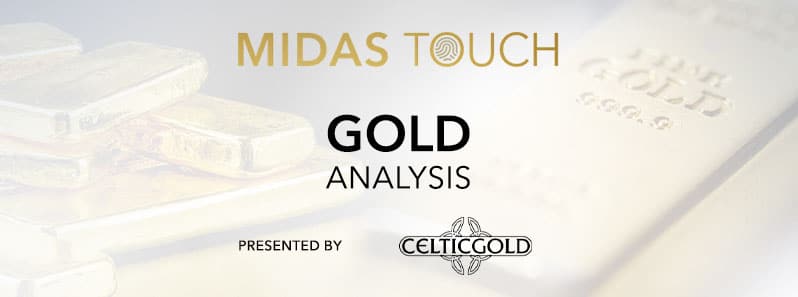

Gold in US-Dollars, monthly chart as of May 5th, 2025. Source: Tradingview

In the IGWT 2024, we initially expected a seasonally typical pullback to below USD 2,200 before the gold rally would continue. However, this pullback did not materialize. Instead, gold prices digested the first leg of the breakout rally with a four-month sideways consolidation at a high level between USD 2,480 and USD 2,280. In May, the sharply rising silver price temporarily added further buying pressure to the gold market. Overall, the situation remained impressively stable and firmly under the control of the bulls.

Unsurprisingly, the gold rally resumed with a breakout above USD 2,500 starting in mid-August and intensifying from mid-September.Supported by a bullish silver price, gold hit a new all-time high of USD 2,790 on October 30th, 2024. This was followed by a sharp sell-off down to USD 2,535 and a seven-week correction, which, as is often typical, took the form of a triangle pattern.

Starting from a higher low of USD 2,580 on December 18th, 2024 – once again timed perfectly with the final FOMC interest rate decision of the year – gold managed to reverse its trend upward. While the start of the next upward wave was somewhat sluggish and uncertain, the bulls took clear control again with a decisive breakout above USD 2,680 from January 10th, 2025. With great confidence and without giving the bears any breathing room, they drove gold prices over the next six weeks to a new all-time high of USD 2,957.

Only then did a sharp pullback to USD 2,832 interrupt the rally for three weeks. After shaking out weak hands and the gold market adjusting to the new price level around USD 2,900, the upward movement continued even more steeply in March. In fact, gold prices rose by 11.83% in four and a half weeks, reaching a new all-time high of USD 3,167. The psychological round number of USD 3,000 posed no obstacle, merely triggering a multi-day consolidation.

“There is no rush like a gold rush” – Well-known saying

Amid collapsing stock markets, however, gold came under severe pressure for a few days starting April 3rd, dropping sharply to USD 2,955. However, after three days, the bearish scare was over. The bulls immediately capitalized on technical support at USD 2,950 to ignite the next price surge. From USD 2,955, the steepest rally yet in the bull market that began in fall 2022 commenced. Within just eleven trading days, gold prices exploded by more than USD 543, or 18.37%, reaching a new all-time high of USD 3,500 on April 22nd!

This new peak, however, marked the start of a significant sell-off on the same trading day, with the notably lower daily closing price of USD 3,380 signaling a clear reversal on the daily chart. Over the next seven trading days, gold dropped significantly by about USD 300.

So far, the support around USD 3,200 has withstood the bears’ initial attack, but an open price gap at around USD 3,175 awaits closure. Additionally, the rapidly rising 50-day moving average (USD 3,094) is still a considerable distance below, confirming the short-term need for correction.

While the daily stochastic has triggered a clear sell signal, the oscillator’s oversold zone remains untouched for now. This suggests that gold bulls will likely need to exercise patience before a reasonably attractive buying opportunity arises due to a strongly oversold condition.

Overall, the overarching uptrend in the gold market remains intact despite short-term fluctuations and increased volatility. The long-anticipated breakout from the large cup-and-handle formation predictably led to a price explosion in the gold market. The strength of the rise over the past 14 months is unsurprising, considering gold had consolidated and corrected for thirteen and a half years prior.

Our price targets of USD 2,535 and USD 3,100 have been fully met. Our next two overarching price targets of USD 4,000 and USD 5,000 are not derived from chart-based projections but from mass psychology. Round price levels often act as psychological barriers or magnets, particularly in uncharted price territories, where many market participants orient themselves.

Naturally, the technical picture across higher timeframes like weekly and monthly charts appears significantly overbought – but this is typical for a pronounced bull market. Nevertheless, a temporary breather until early summer seems plausible, especially since the weekly chart has now generated a sell signal.

It remains intriguing whether gold prices, as seen over the past one and a half years, will primarily correct through a high-level consolidation “over time,” or whether a noticeably deeper and more painful pullback will be necessary this time. For now, we assume the market will lean toward a tricky, sideways consolidation at a high level.

Midas Touch Gold Model™

The Midas Touch Gold Model™ as of May 4th, 2025. Source: Midas Touch Consulting

The Midas Touch Gold Model™ has shifted into bearish mode on April 30th, 2025. While there are also numerous bullish or neutral factors, bearish factors currently predominate. In particular, sell signals on the daily charts for the gold price in US dollars, Indian rupees, and Chinese yuan, as well as a new buy signal for the US dollar, triggered the abrupt trend reversal. This was reinforced—as is typical in May—by the seasonal component, which is now clearly negative for the gold price through June.

Overall, the following conclusions can currently be drawn from the Midas Touch Gold Model™:

- On a broader scale, the buy signal on the monthly chart has been active since February 28th, 2023! A trend reversal would currently only occur if gold prices would fall below USD 2,961. While a correction below USD 3,000 is not out of the question, the bears are currently over USD 350 away from this level. With some luck, the buy signal on the monthly chart could survive the ongoing consolidation/correction and regain strength in a potential summer rally.

- The still-active buy signal on the weekly chart, however, appears significantly more vulnerable. Notably, an open price gap awaits around USD 3,175. The momentum in the weekly stochastic has already turned sharply downward, confirming a stochastic sell signal. As a result, several weeks of sideways to declining prices should now be anticipated. Only when the stochastic oscillator reaches its oversold territory could a multi-week recovery or a direct continuation of the rally become conceivable. In the best-case scenario, gold manages to tenaciously hold above USD 3,000, processing the necessary correction more through time than price. However, the steep price surge in recent weeks also carries the risk of a larger pullback, which could cause significantly more technical damage.

- As physical trading on the Shanghai Gold Exchange and strong physical demand from Asia increasingly drive gold market pricing, the significance of the Commitment of Traders (CoT) report for the gold price has further declined over the past 12 months. Since breaking above USD 3,000, commercial traders have reduced their cumulative net short position to 190,761 contracts in recent weeks, despite gold prices rising by over USD 300 in the same period. Evidently, professionals had to partially close their short positions or deleverage amid the sharply rising prices. Accordingly, open interest in gold futures has also significantly decreased. Overall, the CoT report remains negative.

- The seasonal pattern for the gold market currently signals clear caution, restraint, and, above all, patience. Statistically, the precious metals sector faces an unfavorable phase through July. June, in particular, is traditionally a notably weak month for the gold price.

- Sentiment in the gold market has cooled noticeably after the significant pullback over the past two weeks. However, excessive optimism has been repeatedly observed over the past 14 months. We assume that these recurring phases of sentiment overheating will continue to be corrected by “cold showers”—i.e., short-lived and sometimes sharp price corrections. These typically temporary pullbacks seem to generate sufficient skepticism and restraint among investors without triggering destabilizing overreactions on the downside. Overall, optimism in the gold market is currently neutral, no longer obstructing a continuation of the rally.

Dow Jones/Gold Ratio

DowJones/Gold-Ratio, monthly chart as of May 5th, 2025. Source: Tradingview

- Dow Jones/Gold Ratio: In the long-term comparison, gold has significantly outperformed equity markets, specifically the Dow Jones, since August 1999! This critically important overarching mega-trend remains intact. After an initial strong downward movement of the Dow Jones relative to gold from 1999 to 2011, a notable recovery in favor of US equities followed until autumn 2018. Since then, however, gold has again clearly outperformed US blue-chip stocks. This trend has intensified since early December 2024, with the Dow Jones collapsing relative to the gold price. It is likely that the Dow Jones/Gold ratio will sooner or later retest the low from summer 2011 at 5.73. In the long term, we expect the Dow Jones/Gold ratio to reach approximately 1:1.

- With a gold/silver ratio above 102, silver is historically significantly undervalued, or gold is extremely overvalued. Typically, the ratio fluctuates between 40 and 80. Instead, silver has mostly been trailing gold, slightly dragging down the precious metals sector and mining stocks. A bullish reversal signal would only emerge at a ratio of 90.49, which would require silver to first break above USD 35.

- Due to the weakness of the US dollar and the simultaneous strength of the euro, the gold price trend for investors in the eurozone is less dynamic than for those in the US. While the gold price in USD recently hit new all-time highs, the increase in euros is significantly more moderate. For European investors, this means currency movements can noticeably impact the returns on their gold investments. A strong euro dampens the gold price trend in local currency, potentially causing the impressive gains in the international gold market to arrive muted in the eurozone. This underscores the importance of always monitoring exchange rate developments in precious metal investments. With a new all-time high at EUR 3,036 and current prices around EUR 2,920, however, gold in euros is still solidly up by +15.22% since the start of the year. Nevertheless, for the Midas Touch Gold Model™, only the price performance of the last two weeks matters in the “Gold in the four most important currencies” component. Here, the gold price in euros is slightly negative.

- The sudden shift from a bullish to a bearish model outcome was also driven by signal changes on the daily charts of the gold price in Indian rupees and Chinese yuan. In both currencies, sharp price surges formed prominent flagpole patterns, followed by sharp counter-movements and clear trend reversals. Both charts currently require a strong recovery close to the new all-time highs to reverse the active sell signals.

Gold – Short- to midterm outlook

Gold in US-Dollars, daily chart as of May 5th, 2025. Source: Tradingview

On the daily chart, gold is currently around USD 3,315, approximately USD 185 below the all-time high of USD 3,500 reached on April 22nd. Despite the ongoing Chinese gold rush and massive purchases by numerous central banks, the sharp USD 300 pullback has formed a reversal signal, which could force a tricky consolidation at a high level in the coming weeks.

A significant drop below the psychological USD 3,000 mark, however, seems unlikely. Given the high volatility, nothing can be entirely ruled out. The fundamental drivers of the gold price surge—such as remonetization, geopolitical uncertainties, and the global search for a safe haven—remain present and unresolved, though. We therefore expect a volatile sideways movement with significant fluctuations at an elevated price level clearly above USD 3,000 until early summer. The expected price range is likely between approximately USD 3,050 to USD 3,150 on the downside and USD 3,350 to USD 3,400 on the upside.

Over the course of the year, a continuation of the gold rally with new all-time highs above USD 4,000 would not surprise us. In fact, the gold market uptrend, similar to the period between 1976 and 1980, is likely to accelerate rapidly in the coming months and years, especially as many underinvested investors worldwide continue to chase the already-moving gold train.

This article is our contribution to the In Gold We Trust Report 2025. It was initially written in German on May 4th and 5th, 2025 and then translated into English and partially updated on May 5th, 2024.

Feel free to join us in our free Telegram channel for daily real time data and a great community. If you like to get regular updates on our gold model, precious metals and cryptocurrencies you can also subscribe to our free newsletter.

Disclosure: This article and the content are for informational purposes only and do not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. The views, thoughts and opinions expressed here are the author’s alone. They do not necessarily reflect or represent the views and opinions of Midas Touch Consulting.

{kind=link}

{kind=link}